As Medicare’s annual Open Enrollment period (October 15–December 7) prompts beneficiaries to reassess their coverage options, many older adults are once again weighing the tradeoffs between Medicare Advantage (MA) and Traditional Medicare (TM). For those who prefer the flexibility of TM, one critical factor is access to Medigap— a supplemental insurance that helps cover Medicare’s cost-sharing requirements, such as deductibles, coinsurance, or copayments.

Under federal law, beneficiaries are guaranteed the right to purchase a Medigap plan during specific time periods: within the first six months of turning 65 and enrolling in Part B, within the first year of Medicare enrollment when they switch from an MA plan back to TM (the trial right), or under certain other limited circumstances. In 2022, eighty-nine percent of beneficiaries in TM has some form of supplemental coverage, with 42% enrolled in a Medigap plan.

However, most Medicare beneficiaries lack affordable access to a Medigap plan beyond the initial six months of Part B enrollment and the first year of an MA trial period. Only four states—Connecticut, Maine, Massachusetts, and New York—offer state-level guaranteed-issue protections for Medigap, ensuring beneficiaries can enroll regardless of health status or preexisting conditions. Another four states—Arkansas, Idaho, Vermont, and Washington—require community rating, which prevents premiums from varying based on age or health status. However, because these states do not require guaranteed issue, access to Medigap coverage may be limited outside specific enrollment periods. In all other states, beneficiaries who miss their initial enrollment period or attempt to switch plans after the first-year trial period may be denied coverage or face higher premiums due to medical underwriting.

In this blog post, we address the following question: How do state-level Medigap policies affect MA disenrollment patterns into TM? Specifically, we compare disenrollment rates in the four states with Medigap guaranteed-issue protection versus all other states. We also combine the four guaranteed issue states with states with community rating for Medigap plans in a sensitivity analysis (results available upon request). Because Medicaid typically covers Medicare cost-sharing (premiums, deductibles, copays) and there is little or no demand for Medigap among duals, we excluded dual-eligible individuals and focused our analysis on Medicare-only beneficiaries. Since there is more flexibility for new Medicare enrollees to sign up for a Medigap plan, they were treated as a separate group. Beneficiaries with end-stage renal disease (ESRD) are excluded from all analyses.

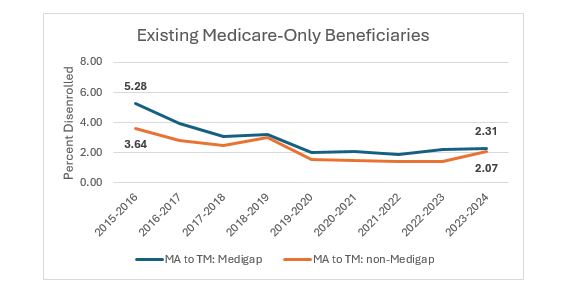

Disenrollment from MA was higher in states with Medigap guaranteed-issue protections, but differences were relatively small in recent years. This trend reflects the reduced financial risk of leaving MA in states with guaranteed-issue or other Medigap protections. MA-to-TM switching declined and then stabilized over the study period in both Medigap states and non-Medigap states. While switching rates slightly increased in 2024 relative to previous year, the differential in switching rates between two types of states in 2024 was small: 2.31% in Medigap states vs 2.07% in non-Medigap states.

Figure 1. Disenrollment Rates from MA Among Existing Medicare-only Beneficiaries

Source: KNG Health analysis of 2015-2024 100% Master Beneficiary Summary File (MBSF) Limited Data Sets.

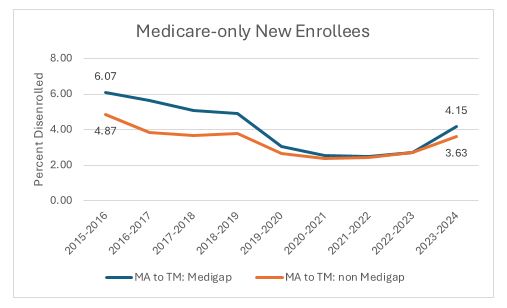

For new Medicare-only enrollees, we anticipated similar MA-to-TM switching across state types due to the one-year federal guaranteed-issue right to Medigap coverage. This is largely true after 2020. In addition, the disenrollment rates in both Medigap and non-Medigap states are substantially higher than rates among existing beneficiaries.

Figure 2. Disenrollment Rates from MA Among Medicare-only New Beneficiaries

Source: KNG Health analysis of 2015-2024 100% Master Beneficiary Summary File (MBSF) Limited Data Sets.

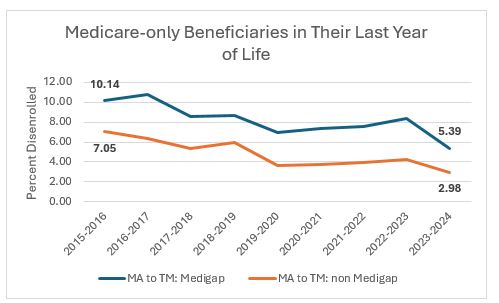

Disenrollment from MA was higher for beneficiaries in their last year of life. The difference in MA disenrollment rates between beneficiaries in their last year of life and all beneficiaries was more pronounced in Medigap states (5.39% vs. 2.31% in 2023-2024) than in non-Medigap states (2.98% vs. 2.07% in 2023-2024). The findings suggest that access to supplemental coverage facilitates transitions for those with intensive healthcare needs.

Figure 3. Disenrollment Rates from MA Among Medicare-only Beneficiaries in their Last Year of Life

Source: KNG Health analysis of 2015-2024 100% Master Beneficiary Summary File (MBSF) Limited Data Sets.

Discussion

Together, these results highlight the complex interplay between policy environments and market forces in shaping Medicare coverage transitions. Among Medicare-only beneficiaries, switching patterns vary with higher MA-to-TM disenrollment in Medigap states, potentially reflecting better access to supplemental coverage outside of MA.

While we expected similar switching patterns for new Medicare beneficiaries across states due to the one-year guaranteed-issue right to Medigap, the trend is only observed after 2020. The elevated switching rates for new beneficiaries, especially in non-Medigap states, suggest that factors such as plan marketing or perceived value may influence early enrollment decisions.

Finally, the higher MA-to-TM switching among beneficiaries in their last year of life, particularly in Medigap states, underscores the potential importance of supplemental coverage availability in facilitating late-life transitions. While such switching may reflect a desire for broader provider access or fewer utilization management barriers, the implications are complex. It remains unclear whether these transitions improve outcomes for seriously ill beneficiaries or primarily reflect dissatisfaction with MA plan restrictions. Moreover, late-life switching may shift the financial burden of high-cost care away from MA plans, potentially driving up Medigap premiums and raising broader concerns about cost and accountability within the Medicare program.

Services : Blog, Payment Policy & Delivery System Innovation Expertise: Medicare, Medicare Advantage, Medigap

|

Dr. Lanlan Xu is a dynamic, results-driven health policy executive with over a decade of experience advancing national healthcare reforms in payment and delivery system innovation, Medicare Advantage, and Medicare & Medicaid alignment. She brings proven expertise in health services research, legislative and regulatory strategy, and cross-sector collaboration, and is a recognized leader in advising senior policymakers on value-based care models and healthcare financing reform. Most recently, Dr. Xu served as Deputy Director of the Division of Health Care Financing Policy (HFP) within the Office of the Assistant Secretary for Planning and Evaluation (ASPE) at the U.S. Department of Health and Human Services. In that role, she led a team of economists and policy analysts focused on Medicare and broader health financing strategies, while overseeing ASPE’s Medicare Advantage portfolio. Previously, at the CMS Innovation Center (CMMI), Dr. Xu led evaluations of large-scale health care delivery models, including the Financial Alignment Initiative for dual eligibles and the Initiative to Reduce Avoidable Hospitalizations among Nursing Facility Residents. Earlier in her career at IMPAQ International (now part of AIR), she led Medicare-focused policy research and evaluations, directed the development of care coordination and quality measures, and supported major CMS models and demonstrations. Dr. Xu holds a Ph.D. in Public Policy from Indiana University and a Ph.D. in German Literature from Georgetown University. |

|

Inna Cintina is a Principal Research Associate in the Evaluation and Health Economics Practice. Dr. Cintina is an applied microeconomist with over a decade of research experience in the area of health economics. At KNG Health, Dr. Cintina is leading evaluations of the impact of managed care on high-need Medicare beneficiaries. Specifically, in work supported by a grant from Arnold Ventures, she is studying the distribution of high-need beneficiaries across enrollment types (Traditional Medicare, Accountable Care Organization (ACOs); and Medicare Advantage (MA)), healthcare services utilization and health outcomes in high-need beneficiaries attributed to ACOs relative to those in MA; and characteristics of MA plans associated with better health outcomes among enrollees. In other work, she studied disparities in utilization of new cardio- and neuro-vascular technologies and impacts of post-acute care settings on beneficiary outcomes. She is an expert in using matching techniques, difference-in-difference methodologies, and other quasi-experimental statistical approaches, as well as producing client-oriented materials, white papers, and manuscripts. She has authored/co-authored more than a dozen articles, which have been published in peer-reviewed journals such as World Bank Economic Review, Health Economics, JAMA, Value in Health, and the American Journal of Managed Care. Prior to joining KNG Health, Dr. Cintina worked at the Lewin Group/OptumServe and the University of Hawaii at Manoa. She has extensive experience in developing and implementing methodologies for identification of causal relationships, advanced analytics, project management, economic burden/cost of illness studies, and impact evaluations of alternative payment models, such as CMMI’s Bundled Payments for Care Improvement Initiative and Oncology Care Model. Dr. Cintina has a PhD in economics from Clemson University, a MSC in European Economics and Public Affairs from University College Dublin, and an MA and a BA in economics from the University of Latvia. |

|

Lane Koenig is President and Founder of KNG Health Consulting and Director of the Healthcare Reform and Payment Innovation Practice. He is a healthcare economist with over 20 years’ experience in the public and private sectors. As President of KNG Health Consulting, Dr. Koenig has overall responsibility for the quality and direction of KNG Health’s research. He serves as Project Director and Principal Investigator for many studies, particularly those related to healthcare reform proposals, healthcare provider payments, value-based purchasing, and delivery system innovations. With expertise on hospital and post-acute care payment and quality issues, his work regularly assesses the potential impact on hospitals and other providers of proposed legislation or regulations. He has assisted both industry and Federal and state governments in the development and assessment of healthcare provider payment policies and value-base purchasing initiatives. Prior to founding KNG Health in 2007, Dr. Koenig was the senior economist in the Office of Policy at the Centers for Medicare & Medicaid Services (CMS). Before joining CMS, Dr. Koenig was a Senior Scientist in the healthcare finance practice at The Lewin Group. Dr. Koenig has led over 100 quantitative and qualitative health policy and health economic studies and has published over 20 peer-reviewed studies in journals, such as Health Affairs, Health Services Research, and Medical Care. He graduated with Honors from the University of Florida, Gainesville and earned his PhD in Economics from the University of Maryland, College Park. |