Accountable Care Organizations (ACOs) and Medicare Advantage (MA) plans have risen to prominence in recent years as two examples of care delivery with enhanced coordination and management of patients’ conditions to improve outcomes. MA plans are privately managed alternatives to Traditional Medicare (TM) offered by insurance companies. ACOs, on the other hand, are networks of healthcare providers that collaborate to provide comprehensive and coordinated care to a specific patient population. While ACOs are part of a fee-for-service payment arrangement, they are also financially rewarded for the savings they generate. There are multiple Medicare ACO models, but Medicare Shared Savings Program (MSSP) remains the largest model, with over 10 million attributed beneficiaries in 2021 (i.e., over 15% of the total Medicare population in 2021). Collectively, the MA and MSSP ACO programs covered 59% of Medicare beneficiaries in 2021. In this piece, we explore whether or not the growth in MSSP ACOs and MA plans has occurred in similar areas of the country.

Growth in MA Enrollment and Beneficiary Alignment with MSSP ACO

In 2016, 46% of eligible Medicare beneficiaries were either enrolled in a MA plan or attributed to an MSSP ACO. As noted above, by 2021, this share had increased to 59%, representing over 37 million beneficiaries. This growth was largely driven by growth in MA enrollment: the share of Medicare beneficiaries enrolled in an MA plan increased from 32% in 2016 to 43% in 2021, averaging a 2-percentage-point change per year. This growth is likely driven by the appeal of supplementary medical benefits (e.g., dental and vision coverage) and non-medical benefits (e.g., transportation, gym memberships, etc.), as well as a high degree of care personalization offered by Special Needs Plans (SNPs) that cater to specific complex populations (i.e., Medicaid-Medicare duals, beneficiaries with chronic conditions and in institutional care). Importantly, unlike Traditional Medicare plans, MA plans have limits on out-of-pocket spending. By contrast, the share of beneficiaries attributed to MSSP ACOs has only slightly changed from 14% in 2016 to 16% in 2021, and generally plateaued after 2018. The slowing growth of MSSP ACOs might be related to changes in the program participation rules that accelerated the transition to two-sided risk, which substantially elevated financial risk for program participants.

Geographic Variation in MA and MSSP ACO Penetration

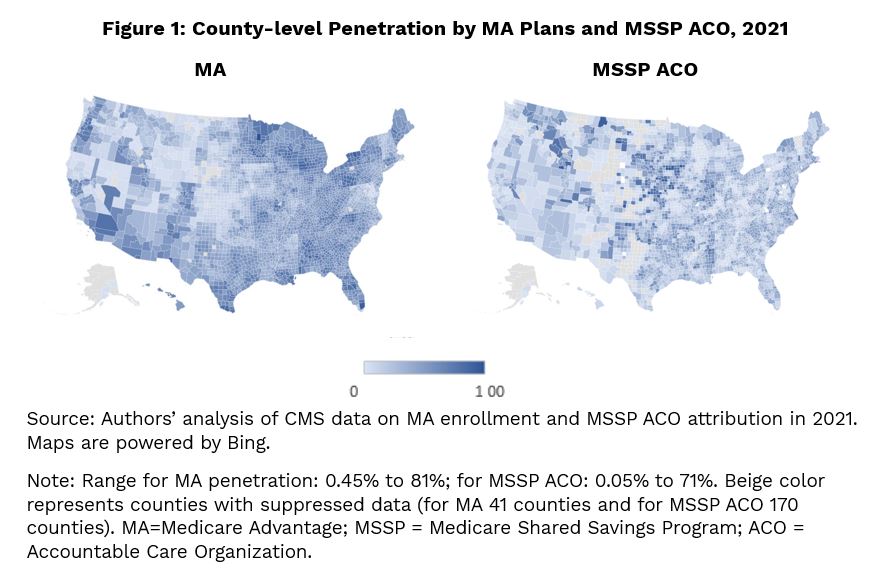

There are substantial regional, as well as county level differences, in penetration rates in 2021 (Figure 1). The MSSP ACO had a higher presence in counties located in the Midwest and Northwest (relative to MSSP ACO penetration in other counties), while MA penetration was more pronounced in counties located in the Northeast and along the East coast. At the state level, Delaware, Nebraska, and Massachusetts had the highest ACO penetration with about one third of their Medicare beneficiaries being attributed to MSSP ACOs. On the other hand, a dozen states had nearly half of their Medicare beneficiaries in an MA plan, with Minnesota and Michigan leading at 53%.

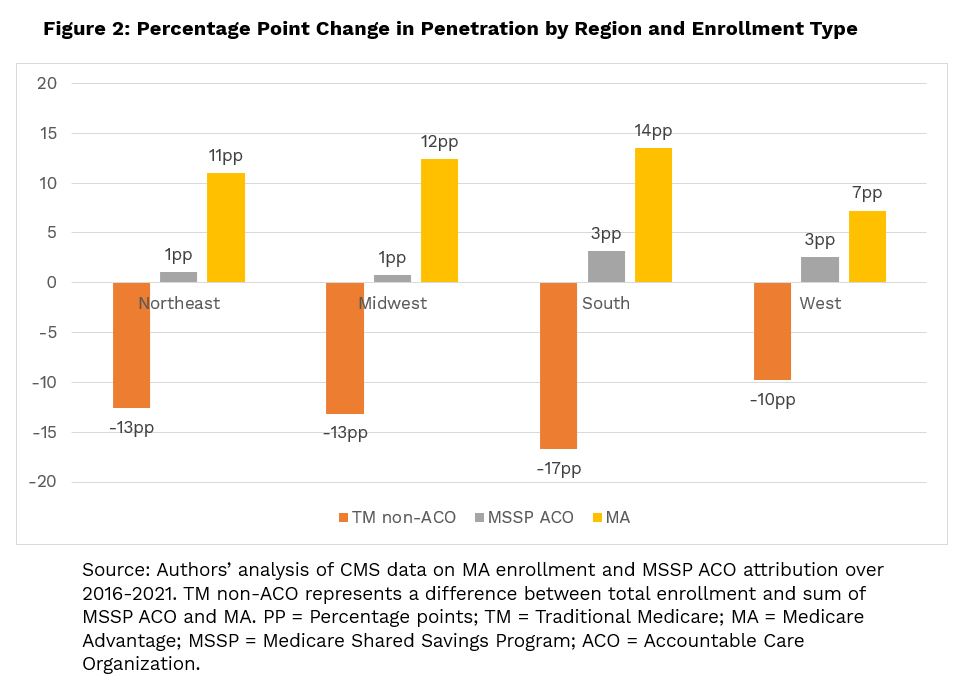

At the regional level (Figure 2), between 2016 and 2021, both programs substantially increased their presence in the South: with a 3-percentage-point change (or 23%) for MSSP ACOs (up from 13.8% in 2016) and a 14-percentage-point change (or 45%) for MA from 29.8% in 2016 to 43.4% in 2021. The higher growth in the South relative to other regions is consistent with previous studies that documented a sharp expansion of MA penetration between 2009 and 2017, especially in the South Atlantic, fueled by the growth of Preferred Provider Organization plans, employer plans, and SNPs. MA also saw relatively larger increases in Midwest and Northeast, which were accompanied by small changes in ACO penetration. The West, on the other hand, saw the slowest growth in MA penetration, relative to other regions, perhaps due to the high level of MA penetration at the beginning of our study period. This region has historically been dominated by health maintenance organization plans, which typically have lower monthly premiums, but do not offer flexibility of coverage for out-of-network care.

Our results show that growth of beneficiaries enrolled in managed care arrangements either via an alignment with MSSP ACO or MA occurred in all markets. Moreover, while regional growth between the two programs varied, there are many markets where there is significant enrollment in both programs. The existence of both options for Medicare beneficiaries in a market could create competition, which could potentially benefit Medicare enrollees. To maximize the benefits from these programs, policymakers need to take steps to foster competition. These include assisting beneficiaries in understanding all their options to receive Medicare benefits, expanding the ability of beneficiaries to enroll in the program and plan of their choice, and providing access to tools and information that allows them to compare options in terms of quality and outcomes.

Services : Blog, Payment Policy & Delivery System Innovation Expertise: Accountable Care Organizations, Medicare, Medicare Advantage

|

Inna Cintina is a Principal Research Associate in the Evaluation and Health Economics Practice. Dr. Cintina is an applied microeconomist with over a decade of research experience in the area of health economics. At KNG Health, Dr. Cintina is leading evaluations of the impact of managed care on high-need Medicare beneficiaries. Specifically, in work supported by a grant from Arnold Ventures, she is studying the distribution of high-need beneficiaries across enrollment types (Traditional Medicare, Accountable Care Organization (ACOs); and Medicare Advantage (MA)), healthcare services utilization and health outcomes in high-need beneficiaries attributed to ACOs relative to those in MA; and characteristics of MA plans associated with better health outcomes among enrollees. In other work, she studied disparities in utilization of new cardio- and neuro-vascular technologies and impacts of post-acute care settings on beneficiary outcomes. She is an expert in using matching techniques, difference-in-difference methodologies, and other quasi-experimental statistical approaches, as well as producing client-oriented materials, white papers, and manuscripts. She has authored/co-authored more than a dozen articles, which have been published in peer-reviewed journals such as World Bank Economic Review, Health Economics, JAMA, Value in Health, and the American Journal of Managed Care. Prior to joining KNG Health, Dr. Cintina worked at the Lewin Group/OptumServe and the University of Hawaii at Manoa. She has extensive experience in developing and implementing methodologies for identification of causal relationships, advanced analytics, project management, economic burden/cost of illness studies, and impact evaluations of alternative payment models, such as CMMI’s Bundled Payments for Care Improvement Initiative and Oncology Care Model. Dr. Cintina has a PhD in economics from Clemson University, a MSC in European Economics and Public Affairs from University College Dublin, and an MA and a BA in economics from the University of Latvia. |

|

Lane Koenig is President and Founder of KNG Health Consulting and Director of the Healthcare Reform and Payment Innovation Practice. He is a healthcare economist with over 20 years’ experience in the public and private sectors. As President of KNG Health Consulting, Dr. Koenig has overall responsibility for the quality and direction of KNG Health’s research. He serves as Project Director and Principal Investigator for many studies, particularly those related to healthcare reform proposals, healthcare provider payments, value-based purchasing, and delivery system innovations. With expertise on hospital and post-acute care payment and quality issues, his work regularly assesses the potential impact on hospitals and other providers of proposed legislation or regulations. He has assisted both industry and Federal and state governments in the development and assessment of healthcare provider payment policies and value-base purchasing initiatives. Prior to founding KNG Health in 2007, Dr. Koenig was the senior economist in the Office of Policy at the Centers for Medicare & Medicaid Services (CMS). Before joining CMS, Dr. Koenig was a Senior Scientist in the healthcare finance practice at The Lewin Group. Dr. Koenig has led over 100 quantitative and qualitative health policy and health economic studies and has published over 20 peer-reviewed studies in journals, such as Health Affairs, Health Services Research, and Medical Care. He graduated with Honors from the University of Florida, Gainesville and earned his PhD in Economics from the University of Maryland, College Park. |